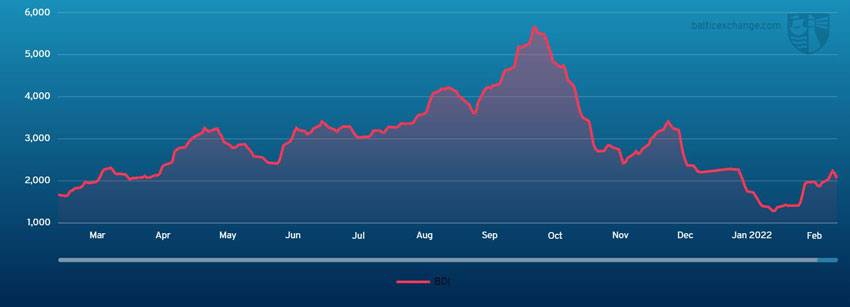

THE Baltic Dry Index last week saw an upturn in the beginning of the week, followed by a slight decline in the later half of the week, as the situation in the Black Sea region deteriorated. However, the BDI still ended higher on Friday than the start of the week.

BDI for Friday 25 February was 2076, this was an increase of 6% on the previous Friday (when the BDI was 1964).

Capesize

The Capesize market did get off to a positive start this week as rates were building strongly off improved sentiment. But as events in Europe took hold, the market abruptly changed course.

The Capesize 5TC reached a high of US$18,181 Wednesday before shedding -4155 by weeks end to close at US$14,026. Increased fuel prices are eating into voyage rate earnings while routes like the West Australia to China C5 closed the last day of the week down -1.505 to US$8.80.

On the ballaster Brazil to China C3 route, rates were also seen to soften to US$21.695 by close of week. The Transpacific C10, where the bulk of Capesize tonnage resides currently, came under heavy pressure settling down -6088 to US$11,154. This is contrast to the Transatlantic C8 which saw only a slight easing down -1125 to US$16,325.

The Capesize market – along with other shipping sectors – now find themselves in the unenviable situation of being cut off from several trade routes due to war risk as vessels are now being halted, turned around and sent sailing in the opposite direction.

Panamax

The Panamax market began the week on a firm footing in both basins.

The Atlantic saw a thinning tonnage list pitted against both a strong mineral demand in the north, alongside healthy grain demand ex NC South America and EC South America. This culminated in stronger numbers fixed. An 84,000-dwt delivery Italy achieving US$21,000 for a transatlantic round trip via NC South America is an indicative mark at that time. These fundamentals remained largely unchanged, until events unfolded in Ukraine on Thursday and put a freeze on this momentum in the Atlantic. As bids were withdrawn/FFA values eroded as the market took stock of potential consequences.

Asia began slowly, but a stable cargo flow ex NoPac/Australia and Indonesia for the most part continued to support rates. An 81,000-dwt delivery North China fixing at US$25,250 for a NoPac round trip. There was a steady appetite for period all week, an 85,000-dwt delivery Korea agreed to US$28,750 for a one-year period.

Ultramax/Supramax

A story of two halves over the week. Whilst from the Asian arena positive movement was seen in most areas, the Atlantic was dominated by the situation unfolding in the Black Sea region.

Period activity was seen, a 63,000-dwt open West Africa fixing a short to medium period with redelivery Atlantic at around US$28,000. The Atlantic was very fluid. A 63,000-dwt fixing a scrap run from the Continent to Turkey at US$17,000, whilst another 63,000-dwt fixed a trip from Central Mediterranean to the Caribbean at US$22,000.

From Asia better levels were seen. A 53,000-dwt open Singapore fixing via Indonesia redelivery China at US$35,000. A 59,000-dwt open Kalimantan area fixing a trip via Indonesia redelivery West Coast India at US$35,000. Stronger levels from the north as well, a 63,000-dwt open Busan fixing a trip to West Africa at US$32,000 for first 70 days and thereafter US$35,000.

There was limited activity from the Indian Ocean, a 62,000-dwt open Calabar fixing a trip via South Africa redelivery China at US$34,000.

Handysize

With the developing situation in the Ukraine, brokers spoke of some uncertainty as to the effects at present. As an ongoing issue it would need to be monitored closely. It was noted by brokers that some owners were now reluctant to call these regions and conwartime clauses were coming into effect.

The US Gulf region continues to firm with a 38,000-dwt fixing from Houston to Italy at US$21,000. East Coast South America is a two-tier market with prompt tonnage softer with a 38,000-dwt fixing and failing a trip from Recalada to the North Continent in the mid US$20,000s.

However, a 38,000-dwt open in March was seen fixing Brazil to the Continent at US$29,000. Asia remains firm with period activity high. A 34,000-dwt fixing from Surabaya for 90 to 120 days with worldwide redelivery at US$34,000 and a 28,000-dwt open in the Arabian Gulf fixing for four to six months at US$26,000.

Clean

In the Middle East Gulf this week the TC1 has begun to show higher freight levels on the LR2s, which are currently marked at WS76.43 and on an upward trend. The LR1s have been active and TC5 55k Middle East Gulf/Japan with more enquiry has seen levels hop up and break the WS100 barrier to WS102.14. The MRs this week saw TC17 retested back up to WS200.42 (-WS3.75), with the round trip TCE at US$10,249/day.

West of Suez, The LR2s, TC15 80k Mediterranean/Japan have had another flat week with little open enquiry and remain at the US$1.85m mark for the moment.

The LR1s, TC16 60k Amsterdam/Offshore Lomé again dropped through lack of activity and are currently around the WS100 mark. On the UK-Continent, MR freight levels have crumbled as the week has gone on. TC2 37k UK-Continent/US Atlantic Coast dropped 23.33 points to WS145, a round trip TCE of US$4695/day. TC19 37k Amsterdam to Lagos has, as usual, followed suit. It fell 25.71 points to WS149.29 (a round trip TCE of US$6803/day).

The Americas have seen another week of improvement of freight with both MR routes once again showing a consistently firming sentiment. TC14 38k US Gulf/UK-Continent is now WS 136.79 (+WS11.08) and TC18 38k from US Gulf/Brazil WS 189.29 (+7.86) a round trip TCE of US$14,029/day.

The MR Atlantic basket TCE fell from US$15,658/day to US$14,618/day. The Baltic Handymax market jumped at the beginning of the week TC9 30k Baltic/UK-Continent is now WS232.86 (+22.86) for the moment. In the Mediterranean, Handymax rates have been edging upwards again all this week. TC6 30kt Skikda/Lavera is now up at WS262.5 (+WS9.06).

VLCC

An upturn all around for the VLCC this week.

In Middle East markets, Rates for 280,000mt Middle East Gulf/USG (via Cape of Good Hope) came up to 19.5 level, while on the 270,000mt Middle East Gulf/China route rates climbed consistently all week to WS38.82 (which shows a round trip TCE of minus US$5800 per day).

At the time of writing WS39 is reported on subjects a couple of times. In the Atlantic, the 260,000mt West Africa/China trip followed a similar pattern of freight level rise all week and presently sits at WS41.18 (a round-trip TCE of minus US$2,504 per day).

A widely reported VLCC fixture for USG/Korea at US$4.95m looks to have led the 270,000mt US Gulf/China trip to be assessed at US$775,000 – higher than a week ago, presently at US$5.1875m (a round-trip TCE of minus US$1,778 per day).

Suezmax

Rates had begun to increase gradually, spiking at the end of the week. TD20, 130,000mt Nigeria/UKC ended up at the WS75 level (a round-trip TCE of approx. US$5800 per day) and TD6 135,000mt Black Sea/Augusta route jumped to WS97.78 (+27.34) (a round-trip TCE of US$16,630 per day). In the Middle East Gulf TD23, 140,000mt Basra/West Mediterranean came up from WS29.69 to WS35.

Aframax

The 80,000mt Ceyhan/Mediterranean rose to WS125.31 (+21.62) (a round-trip TCE of US$15,514 per day. In Northern Europe the rate for 80,000mt Hound Point/UKC is 36.56 points higher than last week at WS133.44 (a round-trip TCE of US$21,710per day). The 100,000mt Baltic/UKC market had the greatest hike of the week of +WS207.5 to WS290 (a round-trip TCE of US$121,741 per day).

On the other side of the Atlantic, the market looks to have plateaued this week 70,000mt EC Mexico/US Gulf was steadfast around the WS160 mark (+/- 2.5 points) a round-trip TCE of around US$24,000 per day. On TD9 the 70,000mt Caribbean/US Gulf route, dipped midweek to WS150 but has now returned to around the WS155 mark returning a round-trip TCE of US$17,250 per day. For the trans-Atlantic route, the rate for 70,000mt US Gulf/UK Continent having started the week fixing in the mid WS130s paused at last done levels (US$12,600 per day round-tip TCE, which becomes a considerably improved figure basis one-way economics).

{kind=link}