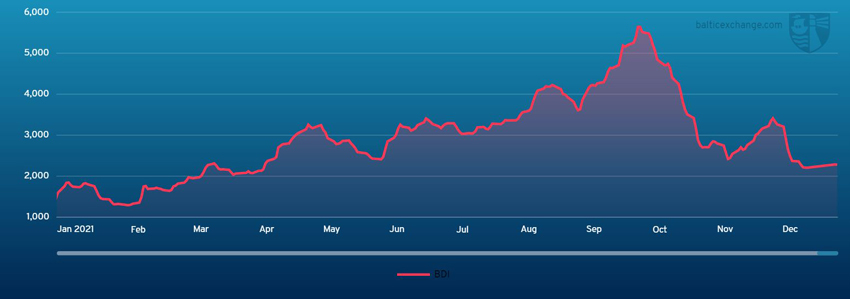

THE Baltic Dry Index was flat over the first week back from the Christmas/New Year holidays.

On Friday (8 January), the index was 2289, was roughly in line with the BDI on Monday 4 January (2285).

Capesize

The Capesize Baltic index returned from year-end holidays this week and immediately saw activity coming from the usual West Australia iron ore flow.

Closing out 2021 at US$19,176 the Cape 5TC ended its first week in 2022 at US$20,167. Initial movement in the market at the beginning of the week appeared positive as physical rates lifted slightly, yet paper markets took the opposite view, leading the 5TC to sink midweek before lifting again for the end of week.

The majority of the weeks trade activity came from the West Australia region to China as the C5 route settled up +.459 Friday to close at US$9632.

Fixtures out of Brazil and the North Atlantic was more muted, as to be expected this time of the year. While activity was low the tightness of vessels in the region was heard to be high as several vessels were having schedule delays leaving the area primed for rate spikes.

The Brazil to China C3 settled for the week at US$21.965 while the Transatlantic C8 priced at US$24,000 – a small premium over the Transpacific C10 at US$18,104. The Capesize paper is showing a small backwardation into February before lifting in March through to the end of the year as optimism for the year holds.

Panamax

Following an uncharacteristic buoyant festive period, the Panamax market commenced the year in true bullish mode – principally due to a fervent EC South America market. This was ably assisted by premium rates being achieved for breaching INL and forcing ice trades in the North Atlantic, US$36,000 was agreed on an 82,000-dwt delivery Hamburg for two laden legs within the Atlantic but this did involve breaching and ice trading. The Asian market this week was essentially supported by EC South America activity with limited demand from Australia and NoPac.

As news announced midweek of an Indonesian coal export ban along with subsequent easing in ECSA demand, sentiment waned, and all markets began to see something of a correction.

Period activity appeared in abundance with a couple of protagonists taking positions, an 82,000-dwt delivery China achieving US$28,500 for five to eight months trading, whilst the same size/type also delivery China agreeing US$26,500 for one year’s trading.

Supramax/Ultramax

After the long break a rather subdued week with many areas seeing tonnage oversupply.

From Asia it was a mixed bag. With the current export ban of coal from Indonesia, rates remained under pressure. Further north, it remained relatively stable with NoPac and Australian business.

Limited fresh opportunities from the Atlantic meant again rates remain under pressure. On the period front, an ultramax open South China was fixed for a short period at around US$26,000.

In the Atlantic, the US Gulf was positional a 56,000-dwt fixing a trip from North Coast south America to the Far East at US$37,000. Whilst from the Mediterranean a 62,000-dwt fixed delivery Çanakkale trip redelivery US Gulf at US$23,000.

From the Indian Ocean it was a little more active. A 58,000-dwt fixing a trip delivery Chittagong via East Coast India redelivery Far East at US$21,500. Further east, a 58,000-dwt fixed delivery Philippines via Australia redelivery Japan at US$22,000.

Handysize

We begin 2022 with the BHSI’s negative trend from last year continuing.

Pressure has been mounting on the Continent with a 32,000-dwt open in Rotterdam fixing basis delivery Poland for a trip to East Coast South America at US$17,000. A 38,000-dwt open in Antwerp fixing for a trip to the US East Coast at US$17,500 with an intended cargo of Steels. A 32,000-dwt was rumoured to have fixed grains from Rouen to the Western Mediterranean at US$14,000.

The US Gulf also has softer sentiment with a 38,000-dwt fixing from New Orleans to Ireland with an intended cargo of grains at US$24,5000.

In Asia, the market has been steady despite the coal ban in Indonesia with a 32,000-dwt fixing from Samalaju via Australia to South China with an intended cargo of Salt at US$23,000. A 34,000-dwt was fixed from Singapore via Kuantan to Guangzhou in the low US$20,000’s with an intended cargo of steels.

VLCC

As we start a new year, we’ve seen a slow take-up the new increased flat rates with most charterers and owners this week maintaining fixtures on the old flat rates. All of the Baltic’s tanker assessments are now based on the 2022 Worldscale though. Activity is ticking over and rates have been relatively flat across the board.

For 280,000mt Middle East Gulf/USG (via Cape of Good Hope) the market is assessed at WS18.5, while 270,000mt Middle East Gulf/China is now a point lower since the start of the year at W37 (showing a round trip TCE of minus US$760 per day).

In the Atlantic region 260,000mt West Africa/China dropped a point to WS37.5 (a round-trip TCE of US$1k/day) and 70,000mt USG/China shed US$20k during the recent few days to US$4.83m (a round-trip TCE of US$2.7k/day).

Suezmax

Rates have been almost static in the West this week with the rate for 130,000mt Nigeria/UKC coming off half a point since Monday to a fraction below WS55 (a round-trip TCE of US$1.6k/day) and 135,000mt Black Sea/Augusta is at the midway point between WS60-62.5 (a round-trip TCE of minus US$3.6k/day).

In the 140,000mt Basra/West Mediterranean market the rate has sunk about four points to WS25 after a few cargoes were covered at this level.

Aframax

The 80,000mt Ceyhan/Mediterranean market softened slightly this week with rates losing four points to the WS82.5 level (a TCE of US$1.5k/day). In Northern Europe rates for 80,000mt Hound Point/UKC fell seven points over the course of the last few days to WS103.5 (a TCE of US$5.7k/day) and 100,000mt Baltic/UKC rates have suffered a nine-point drop to WS120 (a TCE of US$31.8k/day).

However, the returns are still inflated due to the need for Ice-Class vessels. On the other side of the Atlantic fortunes have fared better with 70,000mt US Gulf/UK Continent rising 16 points since Monday to WS106 (a round-trip TCE of US$9.5k/day, improving significantly if calculated basis 1-way economics).

On the shorter-haul markets the 70,000mt Covenas/US Gulf trip is assessed nine points higher at WS97.5 level (US$3.5k/day round-tip TCE) and 70,000mt EC Mexico/US Gulf rates climbed 13 points to WS100 (US$5.6k/day round-trip TCE).

Clean

The CPP tanker market has been settling out this week after the end of the year break. Subsequently almost all markets and sizes have seen rates drop, although the magnitude of which has not been uniform.

In the Middle East Gulf the LR2s of TC1 currently sit at WS98.71 a round trip TCE of US$6976/day and the least impacted of the week at -WS7. The LR1s have been tested the most and TC5 55k Middle East Gulf/Japan is down 14.5 points to WS99.07 a round-trip TCE of US$4126/day. On TC8 a widely reported voyage from this week at US$1.625m has led the index to settle at this level for the moment. The MR run TC17 also dropped WS9.17 to WS179.58.

In the Mediterranean, Handymax vessels have been chipped away at by charterers and TC6 30kt Skikda/Lavera has come off WS10.62 to WS 186.63. The LR2s, TC15 80k Mediterranean/Japan suffered soft sentiment this week and have dropped slightly to around the US$1.87m mark.

The Baltic Handymax has been the most stable market this week and TC9 30k Baltic/UK-Continent has held around the WS220 level.

On the UK-Continent, MR activity has been relatively subdued this week and plenty of available tonnage has seen rates dip. TC2 37k UK-Continent/US Atlantic Coast is currently marked at WS140.28 (-WS4.72) and TC19 37k Amsterdam to Lagos followed suit, dropping 5.36 points to WS144.64 (a round trip TCE of US$9086/day). The LR1s, TC16 60k Amsterdam/Offshore Lomé are untested this week but have dropped off the back of sentiment in the region to WS105.86. In the Americas both runs have been tested down. TC14 38k US Gulf/UK-Continent is now WS 89.64 (-WS11.5) and TC18 38k from US Gulf/Brazil WS 131.79 (-WS6.32).

{kind=link}