INDUSTRY data for May supports the continued small recovery of air cargo volumes but a fall in demand over the last two weeks of the month may signal more challenging times ahead as airlines return capacity to the market.

Having only recently stated that the global air cargo industry had stabilised, but was by no means in good shape, the latest week-by-week analyses by CLIVE Data Services for May pinpoints slightly deteriorating conditions as the month progressed.

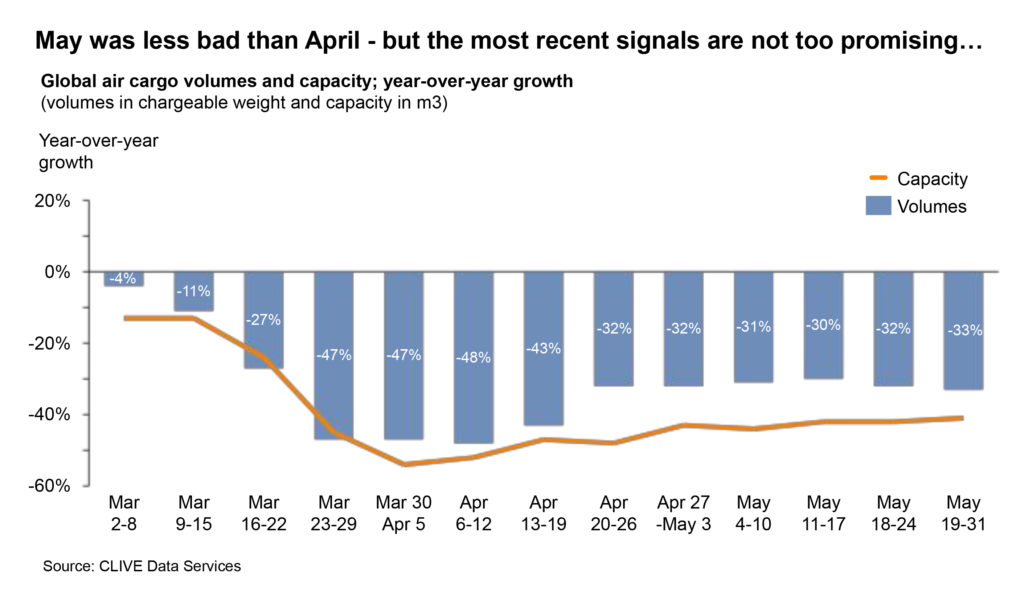

The month of May 2020 was not as bad for the global air cargo industry as April 2020. As hinted in CLIVE’s data last month, the industry has passed the (initial) bottom. After a -37% decline in volumes year-on-year in April, the corresponding figure for May of -31% shows a slight upward curve and, measured alongside a capacity decline of -42% versus last year, the pressure on capacity remained high.

Consequently, CLIVE’s ‘dynamic loadfactor’, based on both the volume and weight perspectives of cargo flown and capacity available, increased month-on-month from 67% to 69%.

CLIVE’s ‘dynamic load factor’ analysis is based on the fact that airlines’ cargo capacity nearly always ‘cube out’ before they ‘weigh out’ as a result of an aircraft’s higher capacity density (available kilograms per cubic metre) than the average density of the goods moved by air.

Consequently, CLIVE says, traditional load factors, based only on weight, underestimate how full planes really are, and thus give a distorted picture of how the industry really is performing.

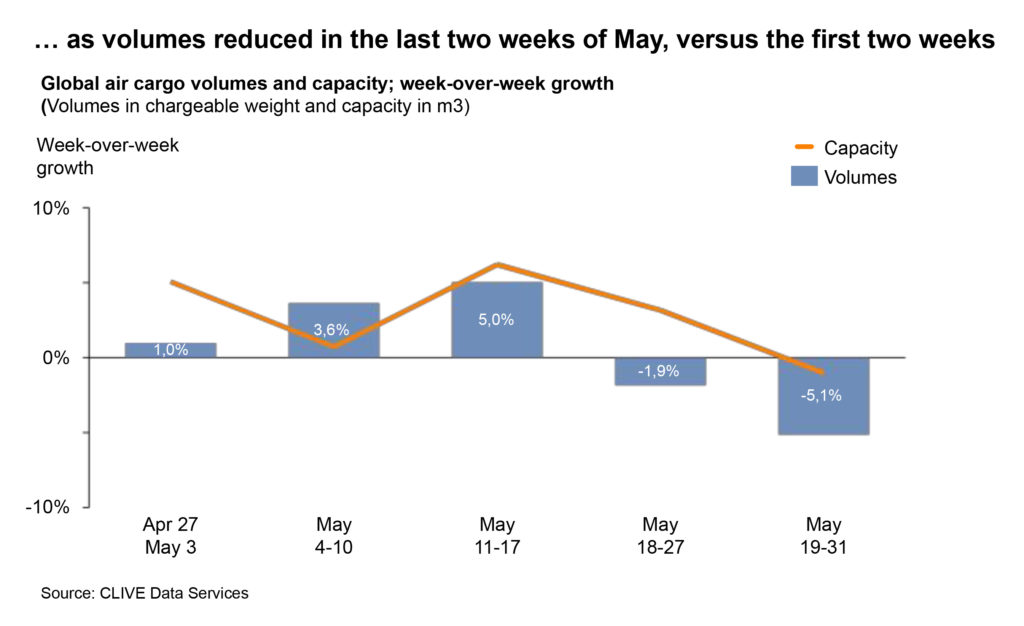

Looking at the most recent weeks, it is clear that May ended weaker than it started. After a series of week-overweek growth in volumes, a decline set in during the week of May 18-24, followed by an even stronger decline for the last week of May. During these last two weeks, the capacity growth rate versus the previous week was higher than the volume growth, thereby reducing the dynamic loadfactor for the first time in weeks by 0.5%. This easing of pressure on capacity had a downward impact on freight rates on major tradelanes, as recently reported by the TAC Index.

“Looking at the last 12 weeks, it is clear to see that market volumes remain erratic and that this will continue for the foreseeable future. This is one of the few certainties we have at the moment,” said CLIVE’s managing director, Niall van de Wouw.

“We can see some dark clouds gathering and this is a cause of concern for air cargo. This is why, in navigating these uncertain times, weekly data becomes not only relevant to decision-making, but crucial.

“Knowing what is happening each week gives the industry the clearest direction. We do not see signals yet that the increase in capacity is being met by growth in demand. With the announcements of increases in passenger schedules, global air cargo revenues may suffer ‘collateral damage’ of more capacity returning to the market,” he said.

{kind=link}