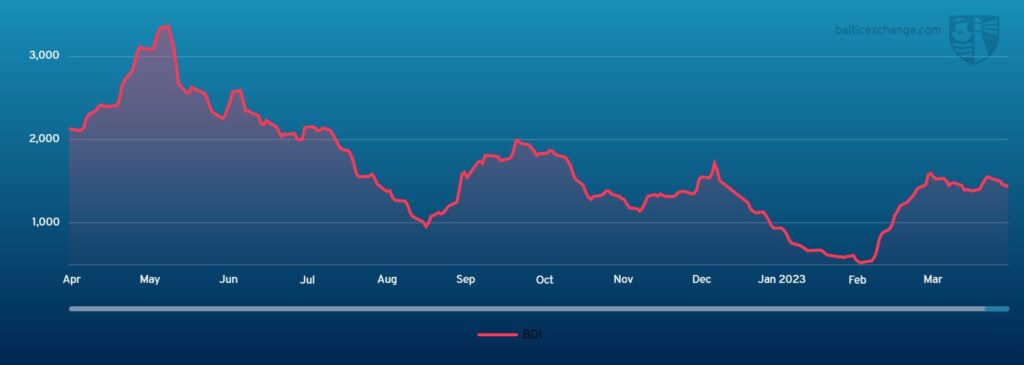

THE BALTIC Dry Index declined over the past week to 1435 on Friday 14 April.

This was an 8% decrease from the previous Thursday’s 1560 (reported ahead of the long weekend).

Capesize

Weather factors in the Pacific this week threatened to disrupt activity from West Australia to China. However, other than Port Hedland closing on Thursday, there was a steady flow of fixing which resulted in a rather volatile week. Several vessels were fixed by the middle of the week from East Coast Australia to China with coal, which offered support to the market at the time. By the end of the week, with these cargoes gone, confidence began to slip as did the rates. The North Atlantic witnessed more activity during the week resulting in less available tonnage and improvement in sentiment. However, the list of ballasters from the Pacific has continued to grow which could potentially cap any upside from South Brazil. There has also been a slight increase in activity from West Africa. All in all, a mixed bag with the 5TC’s starting the week after the Easter weekend at US$15,849 and ending the week at US$15,344.

Panamax

In a week disrupted at both ends by Easter holidays, the market has lost ground and tonnage lists grew in both basins. Overall it was subdued in the Atlantic with Owners having to reduce offers to find cover. A scrubber fitted 82,000-dwt was fixed for a ECSA grain cargo redelivery Skaw-Gib at US$16,250, and a 75,000-dwt fixed for a grain cargo from ECSA for Singapore-Japan at US$17,250. In the Pacific it was a similar story with prompt Indonesian trips covered quickly and a lack of longer duration enquiry. There has been some short period fixing. A 76,000-dwt fixed for four to six months at US$14,000 pd, and a 76,000-dwt fixed for similar period at US$15,800.

Ultramax/Supramax

With widespread holidays both at the beginning and end of the week it was a rather muted affair for the sector. The Atlantic remained rather positional with sentiment remaining relatively strong from the US Gulf and a tightness of larger vessels from the South Atlantic, but other areas lacked fresh impetus. The Asian arena saw sentiment remain soft with limited fresh enquiry from the south and a build-up of prompt tonnage downward pressure on rates remained. Period activity remained limited, although a 54,000-dwt open Indian Ocean was rumoured fixed in the low US$13,000s for one year. Some brokers did say that rate was closer to low US$14,000s. From the Atlantic, a 52,000-dwt fixed delivery United Kingdom trip via Continent with scrap to the East Mediterranean at US$13,000. Elsewhere, a 54,000-dwt fixed delivery Santos for a trip to Malaysia at US$14,000 plus US$400,000 ballast bonus. Asia, saw a 63,0000-dwt open Taichun fix a trip via West Australia with salt redelivery Japan at US$13,400. Otherwise, an Ultramax was heard fixed for a trip delivery Samarinda redelivery full India at US$12,000.

Handysize

In a short week bookended by holidays, visible activity remained limited. The Atlantic showed signs of positivity with brokers speaking of more enquiry in general. In East Coast South America a 38,000-dwt fixed basis delivery when we’re ready San Nicolas for a trip to West Coast South America at US$23,000, whilst another 38,000-dwt fixed basis delivery Rio Grande for a trip to Caldera with an intended cargo of grains at US$22,500. A 43,000-dwt open prompt in Bizerte was rumoured to have been fixed for a trip to the Arabian Gulf at around US$18,500. In Asia, prompt vessels continued to see levels soften with a 37,000-dwt fixing from Japan to Boston-Vera Cruz range at US$11,250. A 39,000-dwt fixed from Sun Duong via Indonesia to China at US$7,000. A 34,000-dwt open in Zhoushan with prompt dates was rumoured to have been placed on subjects for a trip via Eastern Australia to Japan with an intended cargo of sugar in the US$7,000s.

Clean

LR2s in the MEG this week have been balanced with a tip towards a softer dynamic. TC1 has shed five points to WS159.38 (a round trip TCE of US$37,317 /day) and TC20 has had a US$257,000 chunk taken out of it, the index currently sits at US$3,971,429 with reports of US$3,900,000 currently on subjects.

West of Suez, Mediterranean/East LR2s have been relatively sedate this week. Following an early week fixture at US$3,550,000 the TC15 index is currently pegged at US$3,537,500.

In the MEG, LR1 activity has been reportedly low this week. TC5 has shed 7.85 points to WS199.29 and a round trip TCE of US$37,488/day. For a trip West, TC8 has dipped circa US$150,000 to US$3,725,000.

On the UK-Continent, TC16 has improved five points this week to WS175.71 with WS177.5 reported on subjects at time of writing.

MEG MRs have been somewhat fragmented this week with a large influx of enquiry mid-week, including replacements, generating a directionless market. Subsequently the TC17 index has held around the low WS290s all week.

Up on the UK-Continent, activity levels saw a marked uptick this week. As a result The TC2 index has hopped up 35 points to WS250.56 and similarly the TC19 index has jumped 35.71 points to WS260.71.

Over in the Americas, a slower week has dropped the indices over there. TC14 losing 10.83 points to WSWS139.17, TC18 coming down 19.09 points to WS218.33 and a TC21 trip to the Caribbean coming off US$135,000 to US$826,000.

Mediterranean Handymax vessels saw the TC6 index bottom out at WS218 from WS231 to then return to WS225 off the back of improved activity.

Up on the Continent the TC23 index similarly had a big lump (circa 50 points) taken out if it early in the week WS270,s down to WS220s to then return back to WS231.25.

VLCC

The VLCC market showed some optimism this week off the back of a thinner tonnage list, with the exception of the US Gulf to China route. 270,000mt Middle East Gulf to China market saw a 5.05 point improvement taking the index up to WS72.64, which shows an actual rise of about US$6,200 per day with a TCE of US$56,017 basis the Baltic Exchange’s vessel description. The rate for 280,000mt Middle East Gulf to US Gulf (via the cape/cape routing) is assessed at a similarly improved WS47.06 (+W2).

In the Atlantic markets the rate for 260,000mt West Africa/China followed the trend of the MEG seeing the index climb WS1.85 to WS96.95 (a round-trip TCE of about US$52,721 per day, which is US$1,700 per day improvement within a short, post easter, week). The TD22 run, 270,000mt US Gulf/China, is yet to feel the improvements from other regions and the index dipped US$144,000 this week to US$9,950,000 (a round-trip TCE of US$47,159 per day).

Suezmax

The Suezmax market was somewhat fragmented this week and freight rates have slipped. The rate for 135,000mt CPC/Augusta eased an incremental 2.95 points to the WS157.61 mark (a round-trip TCE of about US$78,434 per day). In West Africa, for the 130,000mt Nigeria/Rotterdam voyage, WS115 and WS112.5 were widely reported in the market and the index dropped 10.5 points to WS108.75 (a daily round trip TCE of US$42,254, which is US$7,476 per day less than a week ago). In the Middle East the rate for 140,000mt Basrah/Lavera dropped 2.57 points to WS63.06.

Aframax

In the North Sea market rates for the 80,000mt Hound Point/Wilhelmshaven route dropped about 3.75 points to the WS170 region (a round-trip daily TCE of US$67,018). In the Mediterranean, the rate for 80,000mt Ceyhan/Lavera crumbled about 28 points to around the WS185 mark (a daily round trip TCE of US$59,300). Across the Atlantic, freight for the stateside Aframax vessels has also taken a hit this week. The rate for 70,000mt East Coast Mexico/US Gulf shed around 25 points to WS132.19 (about US$25,643 per day round-trip TCE), while the 70,000mt Covenas/US Gulf has fallen about 16.57 points to W129 (a daily round-trip TCE of US$23,000). For the Transatlantic route of 70,000mt US Gulf/Rotterdam, rates were reduced by 13.12 points to WS138 (rendering a round trip TCE of US$28,104 per day).

LNG

A particularly quiet week for spot LNG with one Unipec cargo reported out of Australia on a 170 CBM vsl in the low US$70,000s in mid May making the market mark for the week on BLNG1g with adjustments for the 160 CBM. BLNG2g and BLNG3g saw some of the lowest adjustments we have with a loss of US$98 on BLNG2g to close at US$40,924, while a BLNG3g run lost US$215 to finish at US$48,596. A bank holiday compounded an already quiet market with rates moving marginally over the week. Sentiment and market activity remains flat and this is expected to continue looking ahead. This week no period rates, which are now available on the website to view, with six month, 12 Months, and 3-Year available.

LPG

Rates on all tree LPG routes have risen, some fixing and potential tighter tonnage has pushed rates higher. Out in the East, rates fared well with an increase of US$3.429 over the week. With cargoes released there was some fixing out into early May with most of April completely covered. The rise in rates pushed TCE earnings up as well from US$55,056 to US$58,354 and sentiment remains positive. The Western markets have seen similar rises, where BLPG3 Houston-Chiba had big gains of US$9.286, a rise of 7.95% over the week. A tight tonnage list with little shown for early May, and mid May onwards still looking tight, supports the recent rise. Charterers have kept cards close to their chest with new stems expected in the coming days. BLPG2 Houston-Flushing rose from US$70.8 to US$74.6 an increase of US$5141 on TCE earnings for a round voyage trip closing at US$77,696.

{kind=link}