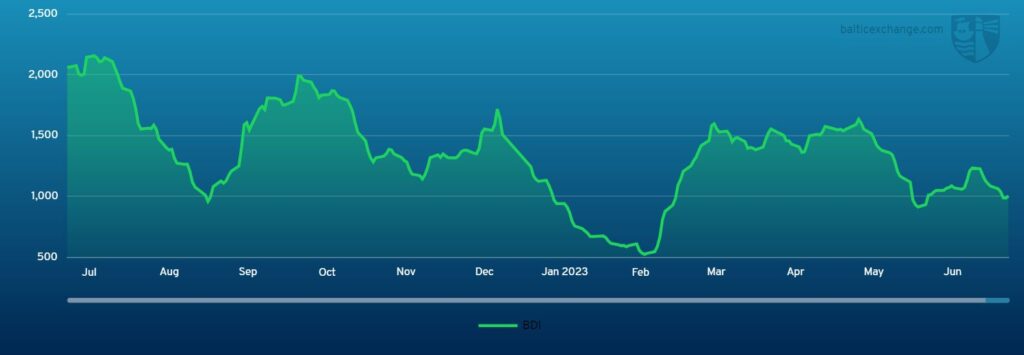

THE BALTIC Dry Index ended last week at 1009. This was down 5.5% on Monday’s index, but up from a low of 993 on Thursday.

Capesize

As the week commenced in the Pacific, it became apparent that there was a notable level of enquiry, defying the usual subdued nature of Mondays.

The majors from West Australia to China have been present in the market throughout the week. However, the market has not been immune to the impact of the increasing tonnage supply as noted by brokers. This began to exert downward pressure on rates at the beginning of the week and the market struggled to gain any momentum. Nevertheless, by the middle of the week market conditions managed to sustain a relatively stable state. As the week approaches its conclusion, a significant number of vessels have been fixed from West Australia to China. As a result, the Pacific has seemingly found a floor.

The Atlantic however, has experienced a lack of notable activity and general enquiry this week, with brokers noting earlier in the week more competitive rates being offered, particularly on the Tubarao to Qingdao route. Concurrently, the bid has also retracted, resulting in downward pressure. However, as the week approaches its end, brokers observed a modest improvement in the Atlantic market overall. All in all, the week has ended on a slightly more positive note.

Panamax

The Panamax market began the week in a slow and depressive state.

Despite the North Atlantic offering reasonable fresh demand, this made insignificant impact to rates with owners keen to take quick cover, discouraging any hope of any rate revival. Notwithstanding this, the north did show some signs of a floor by mid-week as tonnage count tightened and rates on specific trades for now would appear to have bottomed, with an 80,000-dwt delivery Gibraltar agreeing US$6,750 for a grain trans-Atlantic round via NC South America.

Asia returned a further underwhelming week with limited demand, and with the EC South America market offering little solace rates continued to slide. The south of the region saw a steady flow of Indonesia enquiry; however, both NoPac and Australia disappointed again and proved to be the catalyst for further corrections in the market, with reports of an 81,000-dwt delivery Japan fixing at US$8,500 for a trip via EC Australia redelivery Japan.

Ultramax/Supramax

Overall, a poor week for the sector dominated by a strong supply of prompt tonnage and limited fresh enquiry. As the week ended the US Gulf bucked the trend of strong numbers being discussed as a light and more optimistic outlook appeared. Other areas in the basin lacked fresh impetus, once again putting downward pressure on rates. From the Pacific, a similar story as charterers remained in charge and able to cherry pick tonnage. Having said that, some did describe it a fairly positional. Period activity bubbled along, with a 63,000-dwt open SE Asia 8/10 July for one year’s trading in the US$13,000s.

From the Atlantic, a 57,000-dwt was heard to have been fixed from North Brazil to US Gulf in the low US$12,000s. Whilst another 57,000-dwt fixed delivery US Gulf for a trip to the East Mediterranean at US$9,750. From Asia, a 63,000-dwt open South China fixed an Australian round with silica sand at US$12,000. For Indonesian business a 53,000-dwt fixed a trip delivery Xiamen via Indonesia redelivery China in the mid US$5,000s. From the Indian Ocean, a 61,000-dwt was heard to have fixed a trip delivery South Africa redelivery Japan at US$14,500 plus US$145,000 ballast bonus.

Handysize

The issues with a lack of fresh enquiry and general activity across both basins continued this week and the handy sector’s negative sentiment remained. East Coast South America numbers continued to soften with a 36,000-dwt fixing from Rosario to Denmark at a rate between US$11,500 to US$12,000 whilst a 34,000-dwt also opening in Rosario was fixed to the US Gulf with an intended cargo of petcoke at US$13,000. A 35,000-dwt was rumoured to have fixed from SW Pass to Turkey at US$7,000. A 38,000-dwt fixed from Bremen to the US East Coast at US$9,500. In Asia, a 37,000-dwt opening in Japan fixed a trip via Australia back to Japan at US$8,750 and a 35,000-dwt fixed from Japan to Southeast Asia in the low US$6,000s and a 32,000-dwt fixed from Singapore to North China in the US$7,000s. Period was said to still be active and a 28,000-dwt opening in Japan was fixed for three to five months at US$8,500.

Clean

LR2

MEG LR2’s have bounced up and down this week, also seeing TC1 dip to below WS100 for the first time since February. TC1 bottomed out at WS98.06 midweek with reports of a rebound and WS100 currently reported on subjects. TC20 followed suit and lost US$350,000 to US$2762,500 mid-week but is currently marked at US$2,856,250.

West of Suez, Mediterranean/East LR2’s sedate profile continued this week and the TC15 index has been driven down to US$2,275,000, with the Baltic TCE for this firm firmly into negative numbers.

LR1

In the MEG, LR1’s have been tested down this week. TC5 dropped 23.12 points to WS121.88 and similarly a TC8 run shed US$232,050 to be currently pegged at US$2,507,050.

On the UK-Continent, TC16 bottomed out at WS120.94 to then return back up too WS123.5.

MR

MEG MR’s have taken a significant retest down again this week, seeing the TC17 index drop from WS186.07 to WS154.29.

Enquiry has been sporadic this week for the UK-Continent MR’s. As a result freight levels have come under pressure. TC2 has come off 18.75 points to WS141.5 and TC19 has followed, dropping from WS169.38 to WS151.25.

USG MR’s have been little disjointed as the week was bisected by Independence Day bank holiday meaning ultimately freight levels have fallen. TC14 came off 15.83 points to WS116.67 and TC18 dropped from WS215 to WS199.17. A run to the Caribbean on TC21 looks to have most affected shedding US$166,666 to US$704,167.

The MR Atlantic Triangulation Basket TCE dropped from US$27,885 to US$21,841.

Handymax

Mediterranean Handymax’s took a significant leap upwards this week climbing from WS155.56 to WS184.17.

Up on the UK-Continent, TC23 recovered a modest 7.5 points this week to WS129.72.

VLCC

A busier week in this sector, and rates have been pushed down after the mini fightback at the end of last week. In the Middle East, the rate for 270,000 mt Middle East Gulf to China lost about three points since last Friday to WS53.96 (a round-trip TCE of US$32,900/day basis the Baltic Exchange’s vessel description), while the 280,000 mt Middle East Gulf to US Gulf trip (via the cape/cape routing) is now rated one point lower at WS35.81.

In the Atlantic market, the rate for 260,000 mt West Africa/China also dropped three points to WS53.70 (which shows a round voyage TCE of US$33,300/day). The rate for 270,000 mt US Gulf/China is now assessed US$422,223 less than a week ago at US$7,944,444 (US$31,900/day round trip TCE).

Suezmax

Suezmaxes have also had a busier week and again rates have been driven down. In West Africa, for 130,000 mt Nigeria/Rotterdam the rate has dropped another 15 points to WS84.09 (a daily round-trip TCE of US$28,200). In the 135,000 mt CPC/Med market the rate is assessed 4.5 points lower than a week ago at WS107.88 (producing a daily TCE of US$41,000 round-trip) and in the Middle East the rate for 140,000 mt Basra/Lavera lost a further five points to WS50.39.

Aframax

In the North Sea, the rate for the 80,000 mt Hound Point/Wilhelmshaven has hovered around the W130-132.5 mark and published at WS131.43 yesterday (showing a round-trip daily TCE of US$37,000). Meanwhile, in the Mediterranean, the 80,000mt Ceyhan/Lavera rate lost 11 points over the week to WS128.61 (a daily round trip TCE very close to US$31,400).

Across the Atlantic, in the Stateside Aframax market, sentiment remains soft and further rate reductions were made over the week. The rate for 70,000 mt East Coast Mexico/US Gulf fell 21 points to WS127.5 (which shows a TCE of about US$24,600/day round trip) and for 70,000 mt Covenas/US Gulf the rate is 16.5 points lower than last Friday at WS126.88 (showing a round-trip TCE of US$24,000/day). For the trans-Atlantic route of 70,000 mt US Gulf/Rotterdam the rate fell nine points to WS139.38 (a round trip TCE of US$30,600/day).

LNG

The LNG spot market has had a little break from the frenetic fixing of the week prior. Rates for all three routes have been stable with minor fluctuations on all three, resulting mainly from the fluctuations of fuel prices rather than any market activity. For Aus-Japan there was a minimal rise of US$349 on the week to close out at US$67,875. It was reported that the Gladstone LNG plant shipped a total of 28 cargoes in June, a rise of 4.8 %, with most of this volume heading to China. The majority of this is covered via term business so had little effect on spot rates but movement is nonetheless good and sentiment is stable while brokers and owners look towards the upcoming winter market for indicators of potential spikes in freight.

The US saw a similar rise of LNG export with the EIA reporting that 27 LNG carriers departed the US plants in the first week of July, an increase of six from the week before. This rise in export has not affected the indices with the rates staying very stable. Moving between -US$93 and US$370 over the week for BLNG2g and BLNG3g respectively, we published at US$70,591 for BLNG2g Houston-UKC and US$84,261 for Houston-Japan. There has been more focus on the period again where term rates have softened slightly on a one year basis while multi-month ideas gained some traction as traders make sure they have coverage for the winter ahead.

LPG

The gas market has had quite a ride this week. Out in the East there was a steady fall where BLPG1 Ras Tanura-Chiba lost US$19.643 over the week to close below US$100 at US$99.643, which gave a daily TCE earning of US$85,358, over US$20,000 less than at the start of the week. A relatively lengthy tonnage list was not used up enough by the cargoes working and there now seems some overhang looking into August. Rates did take a hit, but it was not unexpected as a correction seemed due while the summer months have been performing remarkably well, but this fall seems to have found its footing and rates have stabilised.

For the US market it was a little more topsy turvy. An initial loss of US$19.715 from the weeks start till midweek had many market participants worried but a rally of fixing and cargoes put a hold on the fall regaining a whole US$10 to close at US$174, which gave a daily TCE earning of US$97,585. Brokers have reported several uncovered cargoes, and a tonnage list that remains tight. This coupled with continued delays in the Panama Canal could rally rates more and the week ahead looks interesting, even while opinions on the direction of the rates is divided.

{kind=link}