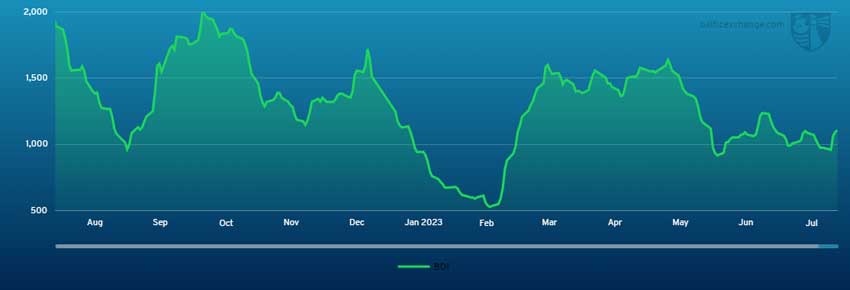

THE BALTIC Dry Index continued its upward trend over the past week hitting 1110 on Friday, 28 July.

The index was 13.5% higher than the previous Friday (21 July), when it sat at 978. Over the subsequent week, the index saw modest gains before falling a few points on Tuesday.

On Wednesday it picked up and increased more than 100 points to round out the week on a high.

Capesize

After a slow beginning to the week, the Capesize market experienced a surge on Wednesday with a rise of over US$2,500 in a day on its five timecharter routes average. The week closed at US$15,180 with +US$3,222 week-on-week. Both fronthaul and trans-Atlantic business were particularly active whilst tonnage in the Atlantic tightened. Solid volume lent support and made the North Atlantic the strongest sector of the week. By Friday, vessels delivered in the Continent/Mediterranean were paid close to US$36,000 for runs to the Far East. From Brazil, moving iron ore to China was marked in the mid US$19s for second half August loading. In the Pacific, the West Australia to Qingdao trade remained stable throughout the week at the level of US$7.70. Currently both a trans-Pacific and a China to Brazil round voyage are in the US$12,000s per day.

Panamax

It was an eventful week with the Panamax market finally finding some life. The week began slowly, but eventually sparked and was duly accompanied by an FFA drive/some Cape splits in parts only to flatten out as the week ended. In the Atlantic, some much needed mineral demand was evident alongside solid demand ex South America for mid/end August arrival window. 82,000-dwt types delivery Singapore were now achieving somewhere between US$10,500 and US$11,000 date dependent. Further north, an 82,000-dwt delivery Continent achieved US$7,500 for a trans-Atlantic round trip via US East Coast. In Asia, rates improved marginally, buoyed somewhat by the pick-up in South America, but decent levels of Australian coal provided the support for most part of the week and a small smattering of NoPac enquiry mid-week, but pitted against a lengthy tonnage list rates hovered around the US$6,000 mark for Australian mineral round trips.

Ultramax/Supramax

Another rather unexciting week for the sector, certainly from the Atlantic, which saw further drops with limited fresh impetus across most areas with the ongoing Summertime slow down. The US Gulf was described as positional whilst the South Atlantic had positional opportunities for owners with prompt vessels, although it did remain fairly uneventful. A 55,000-dwt was heard fixed delivery Recalada for a trip to the East Mediterranean at US$14,000. In the US Gulf, a 58,000-dwt was heard to have fixed from SW Pass to the Mediterranean at US$9,000. From Asia, stronger enquiry was seen in the south at the beginning of the week and with the recent bad weather some vessels where delayed, which kept levels at a reasonable level. Further north, some saw demand remain for backhaul enquiry but limited fresh enquiry was seen from the NoPac. A newbuilding 64,000-dwt open Japan fixed a trip to Brazil in the high US$7,000s. Further south, a 63,000-dwt fixed delivery Koh Si Chang via Indonesia redelivery China at US$9,000.

Handysize

Limited enquiry in the South Atlantic has led to ever growing tonnage availability. A 32,000-dwt was fixed basis delivery Recalada for a trip to the US East Coast with an intended cargo of sugar and duration of about 50 days at US$9,000. The US Gulf was also suffering similar issues with limited cargo availability. A 32,000-dwt was fixed from SW Pass to Israel with an intended cargo of grains at US$5,000 and a 38,000-dwt fixed from Barranquilla to China with an intended cargo of coal at US$10,000. In Asia, a 34,000-dwt opening in Koh Si Chang was fixed for a trip via Kijing to Samalaju with an intended cargo of alumina at US$4,750 and a 37,000-dwt was fixed from Papa New Guinea via Australia for a round voyage at around US$10,000 with an intended cargo of concentrates whilst a 36,000-dwt open in Japan was linked to fixing for a round trip via Australia in the upper US$5,000s.

Clean

The BCTI finished the week at 671, up from 610 the previous week.

In the Middle East Gulf freight rates for LR’s have strengthened with TC1 75k Middle East Gulf/Japan, increasing from WS90.28 to finish the week at WS130.17 (+WS39.89), a round trip TCE of US$26,757/day. This has had a knock-on effect on MRs with TC17, 35kt Middle East Gulf/East Africa, showing similar gains, resulting in an increase of WS46.43 points to WS255 and a round trip TCE of US$29,776/day.

The LR1’s of TC16 60k Amsterdam/Offshore Lomé steadily increased over the course of the week, gaining +WS3.43 points to finish at WS114.06.

West of Suez, on the LR2’s, TC15, 80k Mediterranean/Japan, were mostly flat ending the week at US$2,391,667.

LR1’s have also seen a similar gains over the last week with TC5, 55k Middle East Gulf/Japan, steadily increasing WS37.19 to WS138.75. On TC8 Middle East Gulf/UK-Continent rates softened throughout finishing at 43.30 US$/mt (a lumpsum equivalent of US$2.8m).

Rates for MRs in the US have continued the volatility seen since the beginning of the year, starting off at WS138.33 for TC14 38k US Gulf/UK-Continent, reaching a peak around WS151.25 at the end of the week. TC18 the MR US Gulf/Brazil followed TC14 to end the week at WS228.75 (+7.08). TC21, MR US Gulf/Caribbean, started the week at US$787,500 increasing and peaking at US$945,833 (+US$158,333).

On the UK-Continent, MRs freight levels have been steadily increasing with TC2, 37k UK-Continent/US Atlantic Coast, finishing the week at WS172.75 (+WS13). TC19, 37k Amsterdam to Lagos, followed suit and finished at WS182.5 (+WS13.12).

VLCC

The market in the Middle East softened this week, mostly seen in the earnings rather than fixing rates, while the Atlantic markets gained a little. In the Middle East, the rate for 270,000 mt Middle East Gulf to China yesterday was assessed at WS51.33, a week-on-week drop of 0.7 points, although the daily round-trip TCE of US$27,800 basis the Baltic Exchange’s vessel description is US$3,200 lower than last Friday). The 280,000 mt Middle East Gulf to US Gulf trip (via the cape/cape routing) remained flat in the WS32-32.5 range.

In the Atlantic market, the 260,000 mt West Africa/China rate remained steady around the WS53 mark (which shows a round voyage TCE of US$31,300/day, which is about US$2,000 lower week-on-week). The rate for 270,000 mt US Gulf/China has continued firming and is US$461,111 more than last Friday at US$8,244,444 (about US$33,200/day round trip TCE).

Suezmax

Suezmaxes in West Africa have had another poor week with rates still dropping. For 130,000 mt Nigeria/Rotterdam rates lost another 11 points to settle a little below WS72.5 (a daily round-trip TCE of US$18,300). In the 135,000 mt CPC/Med market, rates are down again, losing a further four points to just above WS90 (showing a daily TCE of US$24,800 round-trip). In the Middle East, the rate for 140,000 mt Basra/Lavera gained a point to almost WS60.

Aframax

In the North Sea, the rate for the 80,000 mt Hound Point/Wilhelmshaven faced a reset in the market and is now assessed 15 points down over the course of the week to WS120.36 (showing a round-trip daily TCE of US$24,100). In the Mediterranean, the rate for 80,000 mt Ceyhan/Lavera is also on a downward trajectory, losing 16 points since last Friday to WS104 (a daily round trip TCE of US$16,100).

Across the Atlantic, in the Stateside Aframax market, rates are tumbling once again. The rate for 70,000 mt East Coast Mexico/US Gulf collapsed 45 points to WS134.69 (which shows a TCE of US$25,700/day round trip) and for 70,000 mt Covenas/US Gulf the rate has tumbled 38 points to WS127.5 (a round-trip TCE of US$22,400/day). The rate for the trans-Atlantic route of 70,000 mt US Gulf/Rotterdam has been chopped by 37 points to WS123.13 (a round trip TCE of close to US$22,400 per day).

LNG

The LNG spot index has not shown much sign of life this last week. Rates are flat while there remains little to no firm spot enquiry. It is summer and expectations were that levels would stagnate. As we look to cargoes being quoted in late September laycans, eyes are once again drawn to the upcoming winter months and what they might bring. It was reported this week by one broker that while term rates have remained steady but high, there has been plenty of interest at inflated levels (vs. spot/multi-month pricing) expectations are that we will once again see the winter spike that we experienced last year. With charterers and traders planning ahead, any potential cargo/stem uncovered or opening up due to a lack of available programmed tonnage could face steep spot rates; something players who have taken tonnage on recently are hoping is the case.

For the actual index minimal changes moved the rates a few hundred dollars only. BLNG1g Aus-Japan fell by US$134 to close at US$68,752, gaining a little back having fallen more than US$500 by midweek. On the Atlantic routes, BLNG2g lost nearly US$750 to finish at US$69,545 while looking east BLNG3g US-Japan rose marginally to close up at US$88,209 having fallen below US$88k mid-week.

LPG

A very quiet week overall where a lack of much enquiry has pushed rates down across all three routes, but it is in the Far East that the greatest fall occurred shaving nearly US$9 off the week’s starting to close at US$99 for Ras Tanura-Chiba. This gives a TCE daily earning of US$83,950 which, though over US$10k off from the start of the week, is still quite healthy earnings for the summer market.

Out in the US rates were steadier. A lack of much enquiry and little change on tonnage availability kept things hovering around the status quo. On our BLPG2 run Houston-Flushing rates fell marginally to close at US$100.2 (a fall of 60 cents from the start of the week). This gives a daily TCE earning of US$114,765. On BLPG3 Houston-Chiba sentiment pushed rates down but not enough to go below US$170. We closed the week at US$170.714 (a fall of US$1.5) and a daily TCE earning of US$94,147 round trip.

{kind=link}